If your company is based outside India—or you’re a foreign investor, a joint venture partner, or an overseas service provider with contracts in India—there’s one banking tool that can quietly transform how you transact in Indian Rupees. And most foreign businesses don’t even know it exists.

It’s called the Special Non-Resident Rupee (SNRR) Account—and after the Reserve Bank of India’s landmark amendments in January 2025, it has become more powerful, more accessible, and more relevant than ever before.

Let’s break it down.

What Exactly is an SNRR Account?

The Special Non-Resident Rupee (SNRR) Account is a dedicated Indian Rupee (INR) bank account that any person or entity resident outside India, with a legitimate business interest in India, can open with an Authorised Dealer (AD) bank—either in India or, now, at the overseas branch of an Indian bank.

Think of it as your official INR gateway into the Indian economy—without the friction of converting foreign currency for every single transaction.

Governed under Schedule 4 of the Foreign Exchange Management (Deposit) Regulations, 2016, and significantly liberalised through the Fifth Amendment Regulations, 2025 (FEMA 5(R)(5)/2025-RB dated January 14, 2025), the SNRR account is now the most versatile rupee account available to foreign entities transacting with India.

Who Can Open an SNRR Account?

The eligibility has been deliberately kept wide. If you have business interest in India, you qualify.

| Who Can Open ✅ |

| Foreign companies with trade or investment activity in India |

| Overseas investors (FDI, ECBs, portfolio investments) |

| Foreign individuals / professionals with service contracts in India |

| Unincorporated Joint Ventures (UJVs) of foreign entities with Indian partners |

| Units in International Financial Services Centres (IFSCs) for transactions outside the IFSC |

| Overseas exporters and importers dealing with Indian counterparts |

| Foreign entities bidding on or executing infrastructure / EPC contracts in India |

No minimum investment. No minimum turnover. No Indian subsidiary required.

You don’t need to set up a company in India. You don’t need a liaison office or branch office. If you have a bonafide business reason to transact in Indian Rupees—an SNRR account is your right.

What Changed in January 2025? (This is the Big Deal)

The RBI’s Fifth Amendment to FEMA Deposit Regulations (January 14, 2025) was a watershed moment. Here’s what changed—and why it matters to you:

| Before January 2025 | After January 2025 |

| SNRR could only be opened with an AD bank in India | Now can be opened at overseas branches of Indian AD banks—in your own country |

| Limited to specific ‘business transactions’ only | Expanded to cover all permissible current and capital account transactions |

| Account validity capped at 7 years | No cap on tenure—the account can last as long as your business in India |

| Transfers only to/from resident accounts | Inter-account transfers between repatriable INR accounts (NRE, NRO, SNRR) now permitted for bonafide transactions |

| Narrow scope—unclear what qualified as ‘business interest’ | Scope explicitly widened: investments, imports/exports, trade credit, ECBs, IFSC business all covered |

In short: the RBI has made the SNRR account longer-lasting, easier to open, broader in scope, and more operationally flexible—all in one amendment. India is sending a clear signal: transact with us in Rupees, on your terms.

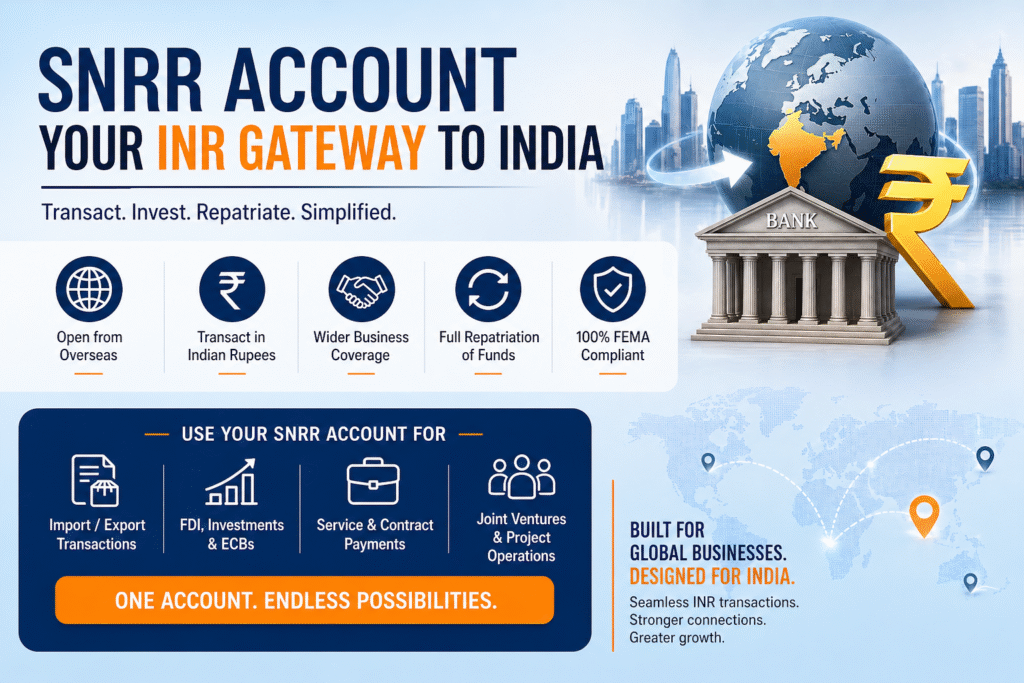

What Can You Actually Do Through an SNRR Account?

Once opened, your SNRR account can be used for a remarkably wide range of India-linked transactions:

Trade Transactions – Receive export proceeds from Indian buyers (in INR) – Pay Indian suppliers for imports (in INR) – Settle trade credit obligations

Capital Account Transactions – Route FDI into Indian companies – Receive dividends, interest, or redemption proceeds – Fund or repay External Commercial Borrowings (ECBs) – Invest in Indian securities under applicable RBI schemes

Services and Contracts – Receive payments for services rendered to Indian companies – Collect income tax refunds from Indian tax authorities – Execute operational payments for contracts being performed in India

For UJVs – Operate day-to-day business transactions of an Unincorporated Joint Venture with an Indian partner – Manage receipts and payments for joint infrastructure or EPC projects

The key rule: The account balance must remain commensurate with your actual business operations in India. It is a transactional account—not a savings or investment parking vehicle.

The Benefits That Actually Move the Needle

| Benefit | Why It Matters to Foreign Entities |

| No currency conversion per transaction | Saves time, forex costs, and hedging risk on every deal |

| Full repatriation of balances | Your INR funds can be freely sent back abroad—no lock-in |

| Open from overseas (post-Jan 2025) | Coordinate with your local Indian bank branch—no India visit required |

| No tenure cap (post-Jan 2025) | Works for long-term projects, JVs, or multi-year contracts |

| Covers all permitted transactions | One account for FDI, trade, ECBs, services—no need for multiple accounts |

| FEMA-compliant by design | Fully within RBI’s regulatory framework—zero compliance ambiguity |

| Useful even without Indian entity | Foreign companies without a subsidiary/branch can still transact in INR legally |

A Practical Example: Why This Matters

Scenario: A German engineering firm wins a ₹200 Crore infrastructure contract in India. The contract involves receiving INR payments from an Indian PSU client, paying Indian subcontractors, and eventually repatriating net profits abroad.

Without SNRR: Every payment cycle involves forex conversions (EUR↔INR), bank correspondent charges, SWIFT delays, and regulatory documentation for each remittance. Operationally painful. Costly.

With SNRR: The German firm opens an SNRR account at the overseas branch of an Indian AD bank in Germany. Client payments credit directly to SNRR in INR. Indian subcontractors are paid in INR from the same account. Repatriation of net proceeds happens seamlessly. One account. Full compliance. Zero forex friction.

Key Operational Rules to Keep in Mind

- ✅ The account must carry a nomenclature specific to the business for which it is opened.

- ✅ Separate SNRR accounts may be needed for distinct business activities (e.g., one for trade, one for FDI).

- ✅ All transactions are taxable in India as per Income Tax provisions.

- ✅ Balances are fully repatriable abroad.

- ❌ No interest is payable on SNRR account balances or linked term deposits.

- ❌ NRO account balances cannot be transferred to SNRR accounts.

- ❌ SNRR accounts cannot be used to provide foreign exchange to Indian residents against rupee reimbursement (round-tripping is prohibited).

SNRR vs. NRO: What’s the Difference?

Many foreign individuals or companies confuse SNRR with NRO accounts. Here’s the quick distinction:

| NRO Account | SNRR Account | |

| Who opens it | NRIs / PIOs for personal income in India | Any non-resident with business interest in India |

| Purpose | Personal income (rent, salary, pension) | Business / investment transactions |

| Repatriation | Restricted (USD 1 million/year limit applies) | Freely repatriable within FEMA norms |

| Tenure | No fixed tenure | Tied to the business / contract duration (no cap post-2025) |

| Target user | Individual NRIs | Foreign companies, investors, JVs |

Bottom line: If you’re a foreign company or a non-resident transacting for business purposes in India, SNRR is the account you want—not NRO.

Why This Matters for India’s Global Trade Ambitions

India’s merchandise and services trade crossed $824.9 billion in exports and $915 billion in imports in FY 2024-25. The government and RBI are actively pushing for INR internationalization—settling more global trade in Rupees, reducing dependence on the USD, and making India a more self-reliant trading power.

The SNRR account is at the heart of this strategy. Every foreign company that opens an SNRR account and transacts in INR is: – Reducing USD dependency in bilateral trade – Lowering transaction costs for both sides – Deepening India’s financial integration with global markets – Benefiting from the natural currency stability that comes with INR-denominated contracts

India is open for business. The SNRR account is how you show up.

How Trade Bridge Advisors Can Help

Navigating the SNRR account process—from eligibility assessment to documentation, AD bank coordination, FEMA compliance structuring, and ongoing regulatory reporting—requires specialists who understand both the legal framework and the on-ground banking realities.

Whether you’re a foreign investor, a multinational exploring India, a JV partner, or an overseas company with Indian contracts—we make your regulatory journey smooth, fast, and fully compliant.

Take the First Step Today

Get your free SNRR consultation with Trade Bridge Advisors.

📞 +91 961-910-2025 📧 info@tradebridgeadvisors.com 🌐 www.tradebridgeadvisors.com

📍 204, Ruparel IRIS, Senapati Bapat Marg, Mumbai – 400 016

Good way of explaining, and fastidious article to take data regarding my presentation subject, which i am going to convey in academy.